HEALTH INSURANCE

Health insurance is a kind of insurance coverage in which the insurer pays for medical and surgical expenses suffered by the insured. This type of insurance compensates the insured for expenses incurred from illness, injury or pays the care provider directly.

With healthcare costs rising at more than 15 per cent a year, having a health insurance is becoming a necessity and we help you manage your health insurance policies that suits your requirement.

We liaise with the leading health insurance providers in India and buying through us enables analyzing costs and benefits from the pool of policies matching your requirements and of course not to forget the quality service offered by us.

HAVE MULTIPLE MEDICAL INSURANCE PLANS? HERE’S HOW TO USE THEM FOR A SINGLE CLAIM

With the rising medical inflation and the increasing costs of hospitalization, the need for a supportive health insurance plan cannot be underestimated. Financial assistance from a health insurance policy can ensure that you receive high-quality treatment without having to pay the high costs involved. * However, in some cases, a single medical insurance policy may not be sufficient. There may be a chronically ill patient within the family, or the sum insured provided by one insurer may not be adequate for the multiple members of a joint family. In such a case, many people often buy dual or multiple health insurance plans for your family. When you have multiple policies, the process to raise a claim can be quite different and a bit more complex than for a single policy. We provide an overview of the same in this article.

RAISING A SINGLE CLAIM ON MULTIPLE HEALTH INSURANCE POLICIES

Two scenarios can occur when you have multiple health insurance policies:

1. THE CLAIM AMOUNT IS HIGHER THAN THE SUM INSURED OF A SINGLE POLICY YOU HOLD

Sometimes, the costs of hospitalization and medical treatment can be quite high, exceeding the sum insured by either of your policies. In such a scenario, you would have to raise claims on both your policies and each would have to contribute with the right balance. * Ideally, you would have a primary policy and a secondary one. You can first raise a claim on the primary policy and claim a high amount. The balance amount would have to be claimed from the secondary policy. For instance, the claim amount is ₹5 lakhs, and your primary health insurance policy has a sum insured of ₹4 lakhs, while the other policy has ₹3 lakhs. Thus, you can claim ₹3 lakhs from one policy and ₹2 lakhs from the other one. 2.THE CLAIM AMOUNT IS LOWER THAN THE SUM INSURED

In this scenario, you can raise a claim on either of the health insurance plans you hold for your family since the sum insured would be lower than the amount you wish to claim. There would be no need for a contribution clause in such a situation.

WHAT TO KEEP IN MIND WHEN BUYING MULTIPLE HEALTH INSURANCE POLICIES?

1. When you are buying more than one plan, you must inform the insurer about the previous policies that you have purchased. If you do not intimate the insurer about the same, it can be considered a violation of the terms. A claim can also be rejected if the insurance company finds out about the other policy during the claim process. 2. To keep the premium of multiple policies stable and balanced, you can use a health insurance premium calculator .This calculator provides an estimate of the premium based on the information you provide, such as your age, gender, smoking habits, policy tenure, sum insured, and so on. 3. Regardless of the number of policies you are buying, you must ensure that each policy and insurance company meets the following parameters:

- Wide range of coverage and add-ons

- A high claim settlement ratio

- A supportive customer service feature

- 24X7 claim assistance service

- A large number of network hospitals

SHOULD YOU BUY MULTIPLE HEALTH INSURANCE PLANS?

Paying premiums for two or more health insurance policies is not an easy matter. Hence, one must decide to buy multiple policies after going through adequate research. The most obvious reason to buy another policy when you already have one is if you are not getting enough sum insured under one policy. There are many reasons for this to occur. For instance, the underwriting principles of the insurer may not allow for a high sum insured if you are buying health insurance at an older age. You may also consider buying another health insurance plan if you are not getting sufficient coverage under one plan. Your family may be covered under one plan, but the diseases/medical events you want coverage for are available under an individual plan from another insurer. It may be a prudent decision to opt for the latter policy in such a situation. Reaching out to a financial expert can also be a great help.

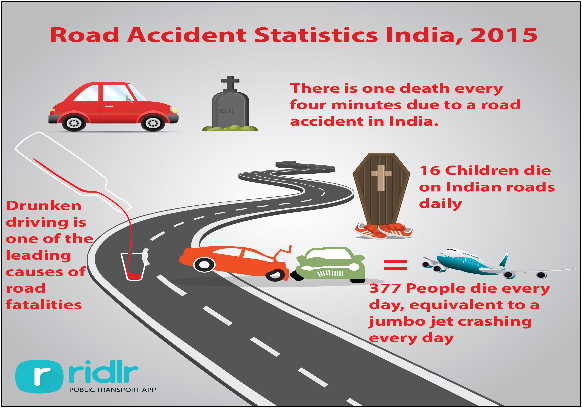

Personal Accident Insurance

Personal Accident Insurance policy provides complete financial protection to the insured members against uncertainties such as accidental death, accidental bodily injuries, and partial/total disabilities, permanent as well as temporary disabilities resulting from an accident. In the case of accidental death of the policyholder, the nominee gets 100% compensation from the insurer. There are various other compensations that are offered for accidental disability such as loss of eyes, limbs, and speech.

Advantages of Personal Accident Insurance Policy

Imagine a situation, you are hit by a motor vehicle and are permanently disabled? There would be no monthly or annual earnings but bank EMIs, medical expenses, and other expenditure. To deal with such an emergency situation, it is advisable to get a personal accident cover. Here’s a quick rundown of some of the major advantages of buying a personal accident insurance policy:

- Family security

- No requirement of medical tests and documentation

- Substantial coverage at a lower premium

- Worldwide coverage

- Both individual and family plans are available

- The easy and certified claim process

- 24×7 support service

- Legal and funeral expenses are covered

- Child education benefit

- Double indemnity for demise/ impairment while traveling in public transport

- Availability of customizable plans

An accident does not come knocking at the door. It can happen anytime, anywhere and may result in minor to serious injuries. Any such uncertainty may lead to financial crisis, and that is why it is recommended to buy a Accidental Insurance policy. It will provide the necessary financial assistance to you and your family against accidental death, bodily injuries and disabilities (Partial/ Permanent/Temporary). There are various other rider benefits such as accidental hospitalization cover, Hospital Confinement Allowance, and Medical Expense Cover.

You can secure yourself against accidental death and disability with personal accident insurance.

Critical Illness Insurance: An Important Safety Measure

A critical illness insurance policy refers to the insurance coverage that helps you to handle expenses related to life-threatening critical illnesses and lifestyle diseases such as cancer, stroke, Parkinson’s disease, paralysis, live disorders, kidney failure, and other ailments etc. These critical illnesses require expensive treatments, which can put financial burden on a person, so it is necessary that these expenses are often covered. And to help you ease your financial pressure, it is essential to get a Critical illness Insurance cover along with the best health insurance policy.